10 March 2025

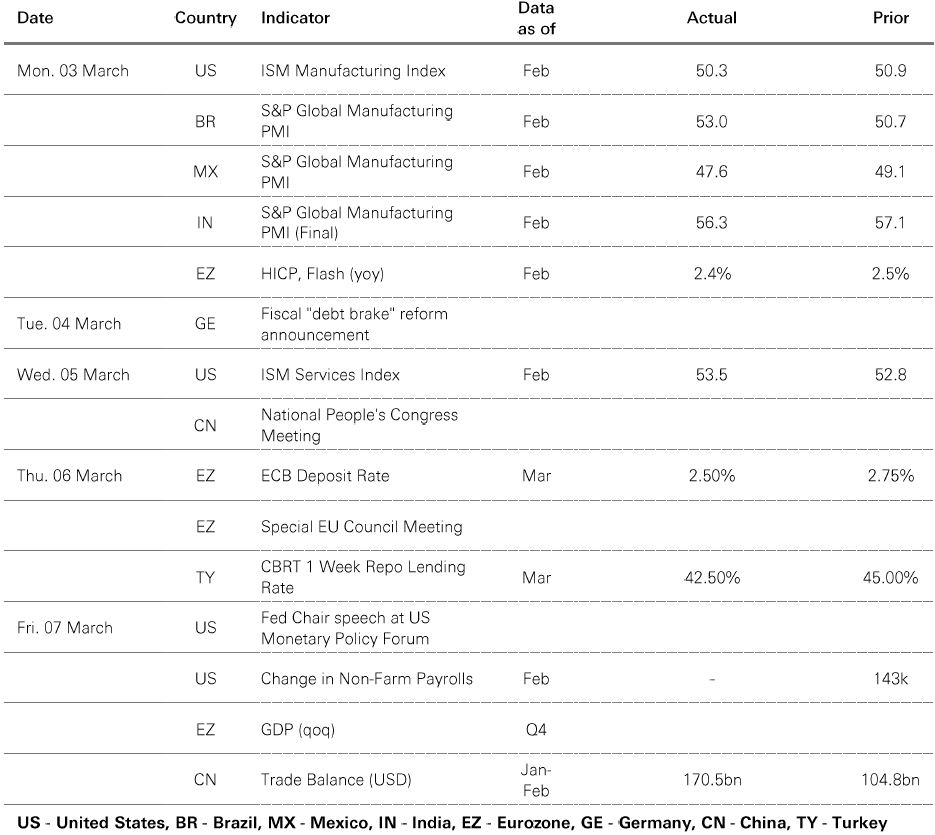

China’s annual National People’s Congress got underway in Beijing last week. Against a backdrop of trade tensions and economic headwinds, all eyes were on further policy support. Premier Li Qiang delivered the government work report outlining fiscal targets and policy priorities for 2025. China is once again targeting GDP growth of “around 5%” this year and has lowered the inflation target to 2%, from 3%, reflecting the country’s low inflation reality.

The overall tone was growth-supportive and market friendly, with the reiteration of “more proactive” fiscal policy and “moderately accommodative” monetary policy. Rather than new stimulus, the emphasis was on policy execution and clearing implementation hurdles (especially for the property sector and local government debt management). For now, China looks set to take a wait-and-see approach to elevated global economic and trade policy uncertainty.

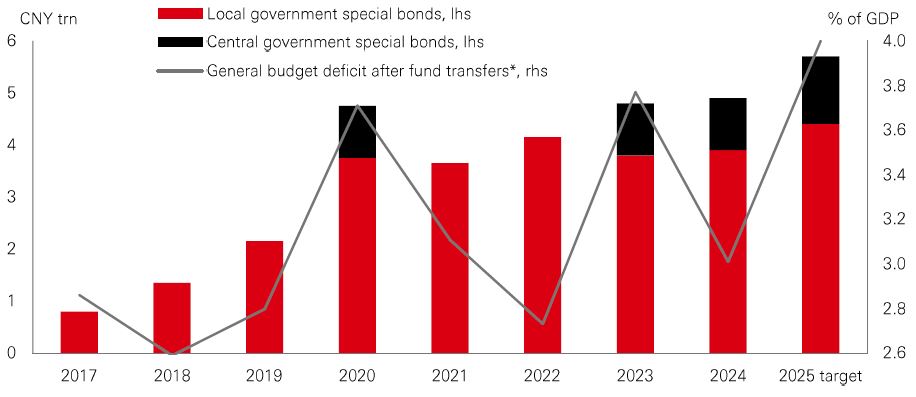

Chinese policymakers have significant policy space to boost domestic demand, if needed. On fiscal targets, the government raised its general budget deficit target to 4.0% of GDP, the widest in decades (up from 3.0% of GDP in 2024). It also plans to issue CNY 1.3trn in ultra-long special treasury bonds (CGBs) this year (up from CNY 1trn in 2024). Local governments will be allowed to issue CNY 4.4trn of new special bonds, up from CNY 3.9trn in 2024.

In terms of policy direction, boosting consumption is now a top priority. There is also a focus on technology innovation and upgrading industry, especially through AI and digital tech. The government also pledged more support for the property sector and the stock market. Overall, the plans confirm a Chinese policy put to support growth. In a global context, it comes amid a fiscal sea change in Europe (see next page) and fading US exceptionalism.

Asian manufacturing PMIs have remained in expansionary territory in recent months, partly reflecting export front-loading ahead of potential US tariffs and some seasonal effects. However, recent surveys also reveal some important country differences. In some cases, the latest sentiment indicators are at odds with stock market performance.

In India, for instance, a composite PMI of 58.8 in February remained firmly in expansion territory, boosted by services activity. Yet the MSCI India index has been Asia’s worst performer in Q1. Other Asian economies like Taiwan and Indonesia have also posted modestly improving +50 PMIs, and they too have seen their stock markets in retreat.

By contrast, PMI data for South Korea showed a shift to contraction territory in February, despite its stock market delivering positive returns this year. While in mainland China, the average January-February manufacturing and composite PMIs, albeit above 50, were marginally lower than their Q4 averages. But mainland Chinese stocks have rallied hard in 2025. Hong Kong equities have also performed well, despite weaker recent PMI readings. So, while PMIs are a useful check on business sentiment, stock markets are driven by more than just macro momentum – sectoral developments, valuations, profits trends, embedded risks, investor sentiment, and even global fund flows all play a part.

* Fund transfers include withdrawals from the stabilisation fund, leftover funds carried forward from past year(s), and transfer from state capital budget and government funds. The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Any views expressed were held at the time of preparation and are subject to change without notice. Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 7.30am UK time 07 March 2025.

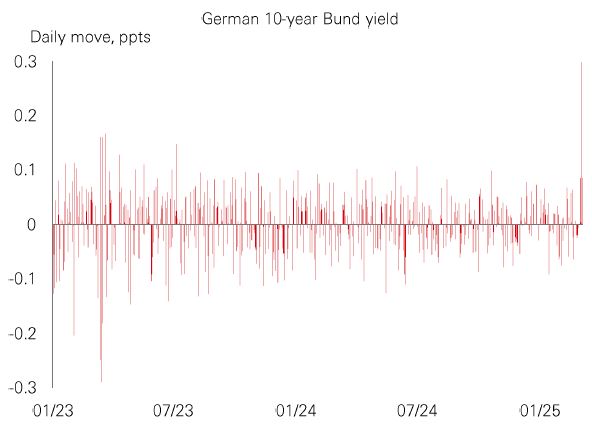

The ECB’s delivery of its widely anticipated sixth 0.25% cut of this cycle was overshadowed by German fiscal developments last week. Borrowing a famous line from the former ECB President Draghi, Chancellor-in-waiting Merz vowed to “do whatever it takes” to defend the country. While proposed changes to the German debt brake to allow for more defence spending are part of the package, the potential game changer is a EUR500bn (c. 12% of GDP) special infrastructure fund. This will be spent over 10 years and is not subject to the debt brake. |

The proposals imply much looser German fiscal policy over the coming years, which should support growth from 2026 (it will take some time for investment projects to get up and running). Bund yields surged by over 0.2% on the announcement, diverging dramatically from the trend in UST yields. Despite this, the Euro Stoxx 50 also jumped by over 2%. Low eurozone growth expectations and eurozone equities trading at a significant discount to the US create a low bar for positive economic and policy surprises to drive further eurozone equity outperformance.

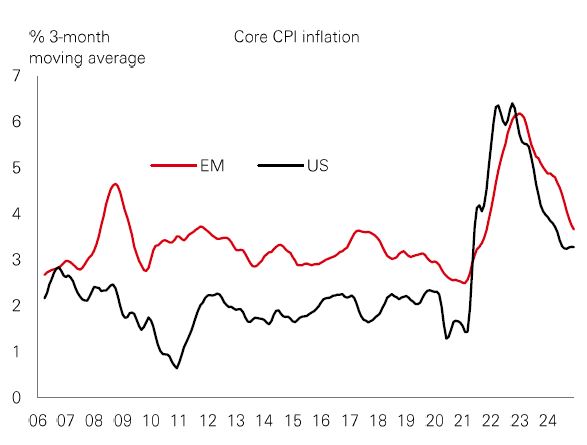

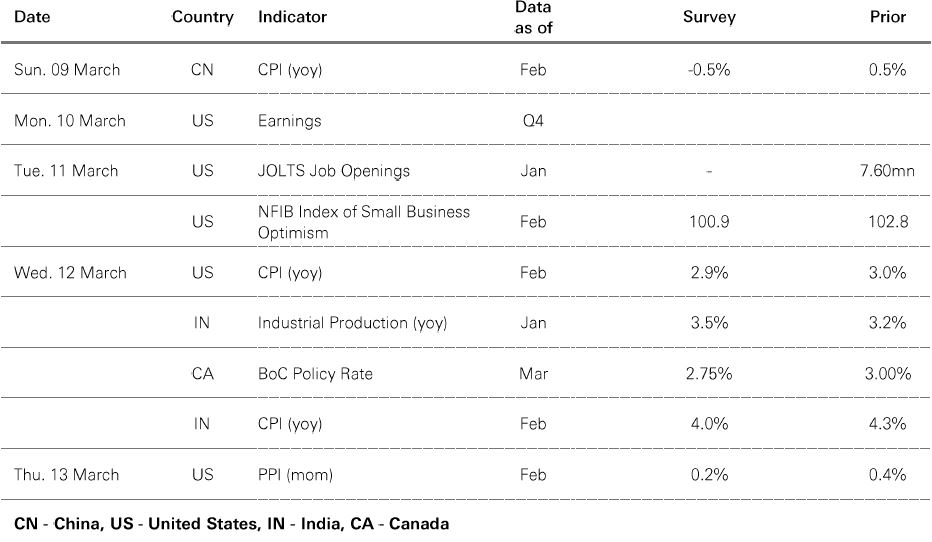

Amid all the recent noise around global trade policy shifts, there has been some positive macro and market developments for the emerging markets universe. First and foremost, in a reversal of well known “Trump trades”, the US dollar has lost ground since the start of the year and US bond yields fell sharply last month. This eases global financial conditions and dollar-denominated debt burdens, and buoys EM currencies. Increasing speculation of a “Mar-a-Lago accord” to weaken the dollar is a reminder that the direction of the greenback isn’t a one-way bet in 2025. Meanwhile, EM underlying inflation continues to freefall, in contrast to US price trends which are displaying signs of stickiness. EM and US inflation could cross paths later this year. Outside of the covid pandemic, this was last seen in 2006 just before “the age of austerity” in the west contributed to keeping inflation rates depressed. |

Overall, these factors provide breathing space for EM central banks to enact further rate cuts, providing a bulwark against external shocks, while helping to unlock value in many EM asset classes. But as usual, a one-size-fits-all approach to assessing the outlook for EMs risks over-simplification, and a selective approach will be crucial.

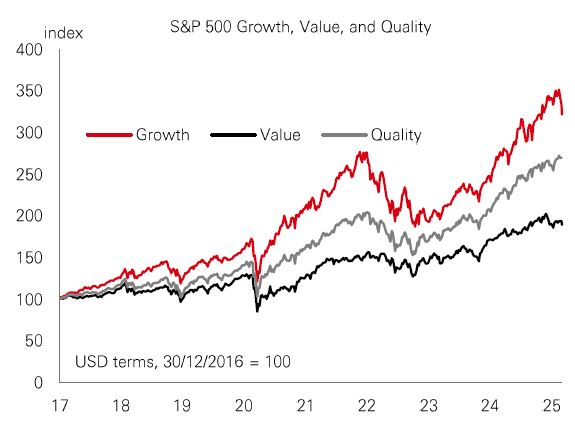

Another bout of episodic volatility in global markets last week continued to weigh on US growth stocks. After a rip-roaring run over 2023 and 2024, the S&P 500 Growth index is down 2.5% year-to-date. Recent Growth weakness is not as extreme as it was in late 2022. Back then, US tech was pummelled by the ramp up in interest rates and the dollar rally that weighed on foreign revenues. The post-pandemic run-up in prices rapidly unwound, with Value proving to be the superior factor, benefiting from higher inflation and rates. So where next for the factors in 2025? While the growth-heavy IT and communication services sectors have seen earnings optimism weaken recently, it could be too early for a material retracement in Growth. AI is likely to remain a significant driver of earnings momentum and interest rates remain on a downward trajectory. |

But recent trends are a reminder that expensive valuations can be a precursor to market volatility. It may also hint at a potential pick-up for left-behind Value. What’s more, in a complex environment where the only certainty is uncertainty, maybe the more resilient and dependable Quality factor could be the winning style in 2025.

Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Any views expressed were held at the time of preparation and are subject to change without notice. Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 7.30am UK time 07 March 2025.

Source: HSBC Asset Management. Data as at 7.30am UK time 07 March 2025. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Risk markets traded mixed amid ongoing concerns regarding US trade policy, with the US dollar index weakening on questions over US “exceptionalism”. In Europe, the ECB lowered rates by 0.25%, with president Lagarde stating that monetary policy was becoming “meaningfully less restrictive”. While US Treasuries were range-bound, a significant shift in German fiscal policy prompted a surge in 10-year German Bund yields, bear steepening the curve, driven by rising supply worries. Among the stock markets, the US saw widespread weakness and underperformed its global peers. The Euro Stoxx 50 index edged higher, as the German DAX rallied and reached a new high. Japan’s Nikkei 225 edged lower as the Japanese yen strengthened. In emerging markets, Asian equities mostly rose, led by the rallies in Chinese equities as policymakers signalled a pro-growth stance at the 2025 NPC meetings. Major Latin American stock markets were up modestly. In commodities, oil fell on rising supply worries, while gold and copper rose.

We’re not trying to sell you any products or services, we’re just sharing information. This information isn’t tailored for you. It’s important you consider a range of factors when making investment decisions, and if you need help, speak to a financial adviser.

As with all investments, historical data shouldn’t be taken as an indication of future performance. We can’t be held responsible for any financial decisions you make because of this information. Investing comes with risks, and there’s a chance you might not get back as much as you put in.

This document provides you with information about markets or economic events. We use publicly available information, which we believe is reliable but we haven’t verified the information so we can’t guarantee its accuracy.

This document belongs to HSBC. You shouldn’t copy, store or share any information in it unless you have written permission from us.

We’ll never share this document in a country where it’s illegal.

This document is prepared by, or on behalf of, HSBC UK Bank Plc, which is owned by HSBC Holdings plc. HSBC’s corporate address is 1 Centenary Square, Birmingham BI IHQ United Kingdom. HSBC UK is governed by the laws of England and Wales. We’re authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the PRA. Our firm reference number is 765112 and our company registration number is 9928412.