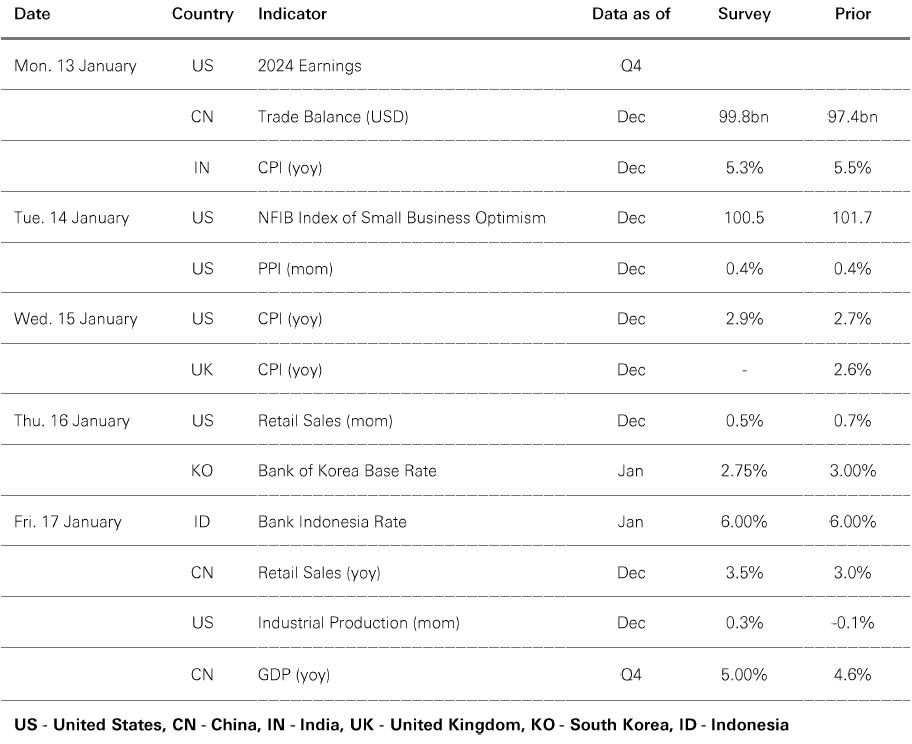

13 January 2025

In 2024, central banks cut rates, fiscal policy remained active, and growth stayed resilient. Many assets – especially stocks and precious metals – did very well. Geopolitics mattered a lot for the market narrative. But (apart from gold), it’s hard to see much evidence of it in 2024 investment market returns.

Megatrends were important in 2024. The AI theme powered growth stocks to outperform value. And the prospect of tax cuts and deregulation turbo-charged investor confidence in US stocks (so called “US exceptionalism”). That all meant that the US market outperformed Europe massively – by more than 20 percentage points in dollar terms.

And bonds put in a decent performance in 2024, unless you were invested in Brazil or Japan. Even so, stocks outperformed Treasuries and other core fixed income assets in 2024 because the macro backdrop of no recession, rate cuts, and profits resilience was simply more equity-friendly.

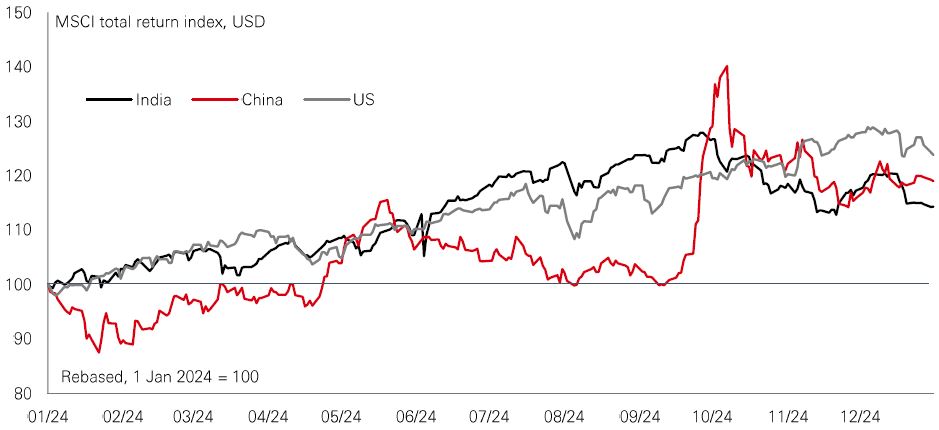

Likewise in emerging markets. Bonds performed reasonably well – with India bonds a highlight. But EM stocks outperformed EM bonds, and the performance of Chinese stocks (outperforming India) was noteworthy (see Page 2). From here, the uncertain macro backdrop looks set to persist in 2025. That’s likely to translate to periods of elevated volatility in markets and calls on investors to do their homework when it comes to asset allocation.

In an unusually uncertain macro environment, making forecasts for the year ahead is even tougher than normal. But here are some of the key macro questions we think will feature heavily in investors’ minds in 2025…

A key question, of course, is which way the narrative on Fed rates will swing next. Could markets even price a Fed hike? And what would that mean for Treasuries, the dollar, and risk assets? Likewise, how will rising policy and geopolitical uncertainty impact trade, global growth, inflation, and investor risk appetite in 2025? With yields rallying at the long end, and signs of term premium rising too, could “bond market vigilantes” play an influential role in disciplining policy makers this year?

And can US exceptionalism keep on going? Will US consumers keep on spending? Can 2024’s market megatrends, like AI, keep on performing? There could be scope for global stock market performance to finally broaden out in 2025, boosting the broader US, European, and Japanese markets. And further policy support in China could be a catalyst to close the valuation discount in Chinese, Asian, and Frontier stocks. There’s certainly plenty for economists and investors to think about at the start of 2025.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Diversification does not ensure a profit or protect against loss. Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 7.30am UK time 10 January 2025.

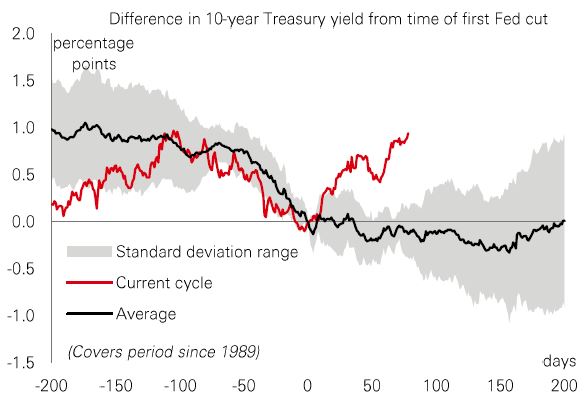

US 10-year US Treasury (UST) yields continued to push higher last week, extending an upward trend that began shortly after the Fed’s first rate cut in September. This defies the textbook crunch lower in yields that usually occurs after the Fed starts to lower rates. Structural, rather than cyclical, factors appear to be driving the sell-off. Activity data have been in line with expectations and the latest core PCE inflation number was on the low side. To some analysts, the move reflects a mix of markets pricing in a higher neutral policy rate, given the resilience of growth; and increasing concerns about US government debt dynamics. |

The base case is that some moderation in US growth and inflation allow the Fed to ease 0.50%-1.00% in 2025, limiting the scope for a significant further sell-off in USTs. However, the situation warrants close attention. As well as weighing on growth prospects and raising financial stability risks, rising UST yields can create problems in other markets. For example, since early December, the equal-weighted S&P 500 is significantly down, while longer-dated UK gilts have underperformed USTs, reflecting the UK’s stretched fiscal position and weak growth.

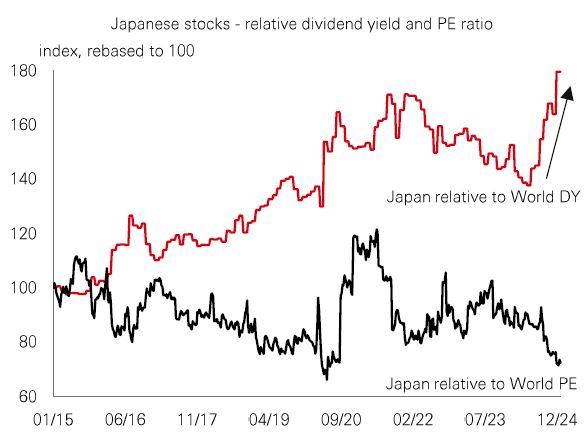

Japanese stocks underperformed global peers in dollar terms in Q4 2024. Potential changes in US trade policy, plus the strength of US stocks and the dollar influenced the performance. Domestic forces were also at play, with uncertainty over the timing of Bank of Japan rate hikes. Yet, the outlook for Japanese stocks is potentially positive for three reasons. First is that Japan continues to shift from prolonged disinflation to reflation, with consensus nominal GDP rising to 3.3% this year. Second, initiatives to boost corporate governance continue, with firms hiking shareholder payouts (dividends and buybacks), leading to fitter balance sheets and higher return on equity (ROE). |

Third, Japanese valuations have not kept pace. Not only have price-to-book values lagged the broad rise in ROE, but there has also been a substantial pick-up in dividend yields, which are up by close to 80% over the past decade on a relative basis. During the same period, 12m forward relative price-earnings (PE) ratios have also declined, leaving Japanese stocks trading at 14.5x versus the world on 18x. That could offer a compelling entry point for investors.

Chinese stocks delivered double-digit gains in 2024, with the market outperforming major regional neighbours like India and South Korea. That was largely driven by a leap in valuations after a fresh round of economic and market stimulus measures last September. Yet, Chinese markets have been weak of late. Investors are fretting over headwinds ranging from lacklustre domestic demand and geopolitical risks to the strong US dollar and the prospect of tariffs. There is also uncertainty over the timing and scope of further domestic policy support. |

On that front, parliamentary sessions in early March could see details on the 2025 growth and fiscal deficit target, the annual bond issuance quota, and other economic and social targets. Officials have already set a pro-growth policy tone for 2025. More demand-side stimulus, further efforts to stabilise the property sector, and structural reforms to rebalance the economy could support the growth outlook. For investors, Chinese stocks continue to trade at a discount despite analysts being optimistic on the profits outlook. Any positive news following the March meetings could boost sentiment and foreign inflows.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. Diversification does not ensure a profit or protect against loss. Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 7.30am UK time 10 January 2025.

Source: HSBC Asset Management. Data as at 7.30am UK time 10 January 2025. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

A widespread sell-off in core government bonds stifled risk markets amid ongoing uncertainty over US trade policy and the rate outlook. The US dollar continued to strengthen against major currencies. Gilts lagged behind Treasuries and Bunds due to rising UK fiscal concerns, with poor investor demand for the latest 30-year Gilt auction. US equities struggled to make headway ahead of the Q4 2024 earnings season. Europe’s Stoxx 50 index began the year on a positive note, but Japan’s Nikkei 225 tracked US stocks lower. In other Asian markets, Hong Kong’s Hang Seng fell, led by losses in some tech heavyweights on lingering worries over geopolitical tensions. Mainland China’s Shanghai Composite also slid, and earnings worries put pressure on India’s Sensex. Korea’s Kospi index bucked the trend, aided by stronger tech shares. In commodities, gold and copper advanced, while oil remained firm.

We’re not trying to sell you any products or services, we’re just sharing information. This information isn’t tailored for you. It’s important you consider a range of factors when making investment decisions, and if you need help, speak to a financial adviser.

As with all investments, historical data shouldn’t be taken as an indication of future performance. We can’t be held responsible for any financial decisions you make because of this information. Investing comes with risks, and there’s a chance you might not get back as much as you put in.

This document provides you with information about markets or economic events. We use publicly available information, which we believe is reliable but we haven’t verified the information so we can’t guarantee its accuracy.

This document belongs to HSBC. You shouldn’t copy, store or share any information in it unless you have written permission from us.

We’ll never share this document in a country where it’s illegal.

This document is prepared by, or on behalf of, HSBC UK Bank Plc, which is owned by HSBC Holdings plc. HSBC’s corporate address is 1 Centenary Square, Birmingham BI IHQ United Kingdom. HSBC UK is governed by the laws of England and Wales. We’re authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the PRA. Our firm reference number is 765112 and our company registration number is 9928412.