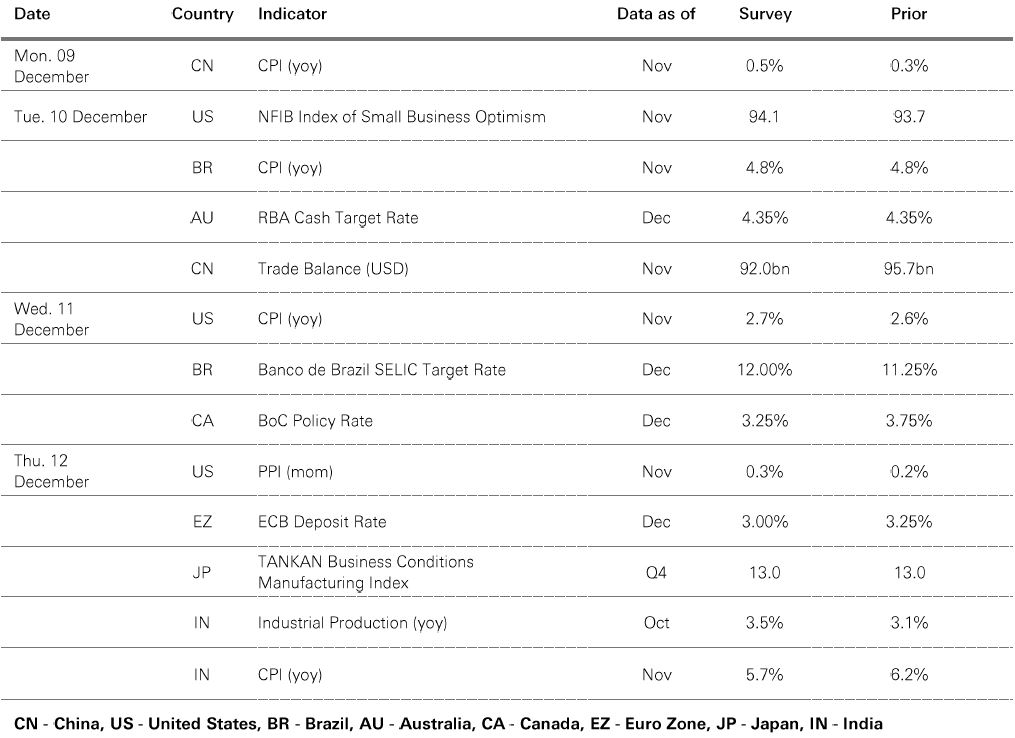

9 December 2024

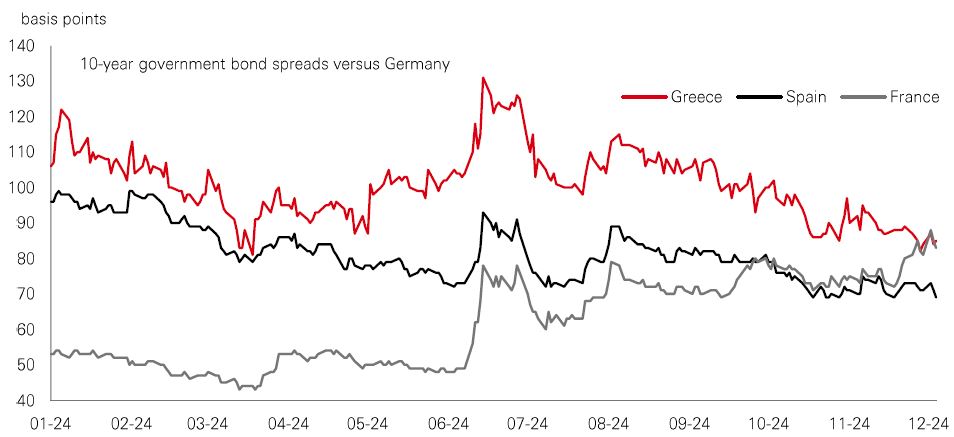

Are good economics now bad politics? Recent developments in France are a case in point. IMF forecasts show the country’s public finances are on an unsustainable path, with the debt ratio expected to reach almost 130% of GDP by the end of the decade. But with the French parliament split into three blocs, there is limited political will to find a solution. French Prime Minister Barnier’s proposed EUR60bn budget consolidation saw him swiftly ejected from office.

Amid the political impasse, France’s 10-year government bond spread over Germany has moved higher, and is now above that of Spain and Portugal. Yet, this is not a marker of an imminent crisis. In the words of financial wags, it's not a “Truss moment”. Spreads in France have not blown out in the same way they did in the UK in September 2022, when then-Prime Minster Truss introduced a budget that incorporated significant unfinanced tax cuts, worsening debt sustainability. No such measures are being touted in France for the time being.

The market reaction to last week's events in France has been sanguine. That reflects today's better economic reality versus 2022 – ongoing disinflation, central bank rate cuts, and decent global growth. The ECB also provides an ultimate backstop against disorderly market dynamics in the eurozone via the Transmission Protection Instrument (TPI), even if this comes with strings attached. So, although events require monitoring, and the distinction between the eurozone core and periphery is blurring, this is likely to be a slow-burn issue rather than the start of a new crisis.

With inflation remaining a bit sticky in places, and fiscal activism still in play, it makes sense that investors expect a fairly shallow rate cutting cycle in 2025. The ability of central banks to insulate the economy and markets against adverse shocks – the so called “Fed put” – looks constrained.

We think many alternative asset classes offer an attractive solution. Hedge funds, for example, have exhibited consistently low correlations to stocks over the past three years. This coincides with a period of higher rates and a higher dispersion of equity returns which typically benefits “stock picking” strategies that hedge funds embed. This contrasts with the 2010s when record-low interest rates were causing nearly all stocks to rise in unison. For 2025, an environment of rising uncertainty and market volatility would likely to keep dispersion high. And for those hedge funds with significant unencumbered cash balances, higher rates would provide a further boost to their total return.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Diversification does not ensure a profit or protect against loss. Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 7.30am UK time 06 December 2024.

Barring a major shock between now and the new year, US stock markets are set to notch up world beating performance in 2024. To many, this comes as no surprise in a year where the soft landing was delivered, profit growth rebounded, and AI started delivering on its huge potential. But where does this leave us for 2025?

We think US markets can continue to perform well. The prospects of tax cuts and deregulation is the icing on top of the cake that is a resilient US economy. Profit growth is likely to remain strong, even if current expectations of c. 15% for 2025 EPS growth look somewhat optimistic.

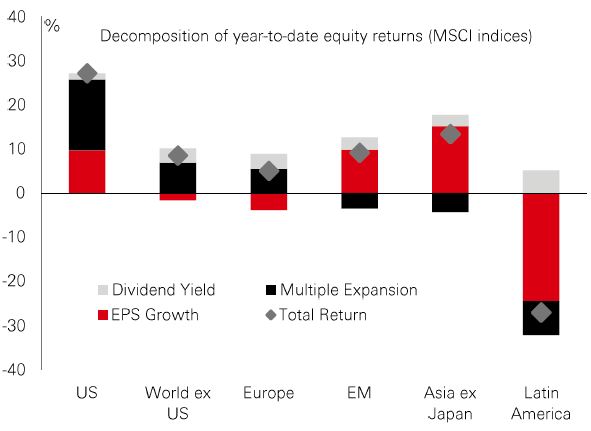

But a key challenge will be valuations. Decomposing year-to-date equity returns shows multiple expansion has been responsible for the bulk of US gains this year, unlike in emerging markets – particularly in Asia - where profits and dividends have driven stocks higher. This leave US stocks trading on a 12-month forward PE of 22.0x, well above the last 10-year average of 18.6x. Stretched US valuations, along with a “broadening out” of profit growth across the world, make it important to look beyond recent winners.

Despite a good start to 2024, European equities have struggled for momentum since the summer, while US stocks have zipped ahead. Year-to-date, this leaves European stocks experiencing their worst relative performance to the US in close to 50 years.

Investor pessimism around Europe is perhaps unsurprising. The export-dependent bloc is weighed down by weak global trade growth, exposure to soft Chinese demand, and competition from China’s lower cost carmakers. German Fortune 500 companies have announced over 60,000 layoffs this year with more expected to come. On top of the bad economic news, the region’s politics looks troubling (see main story).

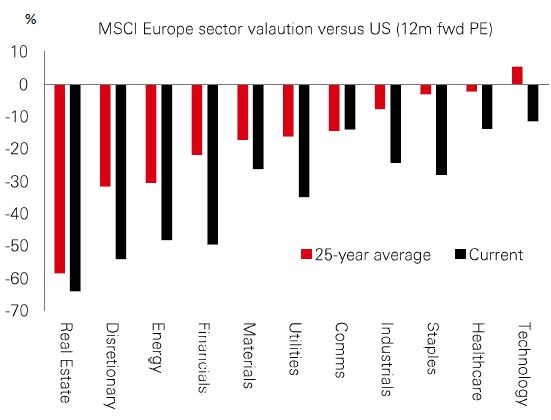

The outcome is a European market that now looks very cheap. MSCI Europe is on a trailing PE of 15.3x versus 30x for the US. At the sector level, discounts look particularly pronounced for consumer staples, healthcare, financials and industrials. So, although caution is warranted, some re-rating is possible – triggered perhaps by scope for China’s reflation, or government support for domestic “world-class” brands. A weaker euro helps. And bargain hunters are likely to be out in force, making M&A and buyback activity a potential boost in 2025.

2024 has been a great year for Asia’s credit markets, especially for high-yield bonds. The benchmark JACI high-yield index has delivered double-digit returns. Following a tough period for the market post-pandemic, several factors have reignited investor enthusiasm.

Firstly, exposure to China has fallen considerably as troubled real estate names have defaulted and dropped off indices. This “flushing out” process has resulted in a market that is not only more geographically and sectorally diverse, but also has a much lower average default rate. Many companies now operate with healthy balance sheets and easy access to cheap local funding channels.

This leaves the asset class in a strong position for 2025. Yields remain higher versus historical levels and DM equivalents, providing room for further spread compression. Of course, China’s macro situation is a key risk to monitor, and there is likely to be noise around tariffs. But improved diversification – including increased exposure to fast-growing India – and ongoing China’s stimulus measures should limit the downside.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Source: JP Morgan, HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 7.30am UK time 06 December 2024.

Source: HSBC Asset Management. Data as at 7.30am UK time 06 December 2024. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Positive risk market appetite persists despite increased political tensions, and the US Dollar index consolidated. Core government bonds were range-bound, as Fed Chair Powell stated the Fed “can afford to be a little more cautious” on the path to a neutral policy stance. In US equities, the S&P500 touched an all-time high but lagged the Nasdaq. The Euro Stoxx 50 rallied, with France’s CAC rebounding. The Nikkei 225 strengthened on higher machinery makers as the yen traded sideways (vs USD). EM stock markets were broadly higher, led by India’s Sensex index. The Shanghai Composite and Hang Seng advanced ahead of China’s Central Economic Work Conference whereas rising political worries weighed on South Korea’s Kospi index. In commodities, oil edged higher as the OPEC+’s decided to delay a plan to roll back production cuts to April 2025. Gold edged lower, while copper gained.

We’re not trying to sell you any products or services, we’re just sharing information. This information isn’t tailored for you. It’s important you consider a range of factors when making investment decisions, and if you need help, speak to a financial adviser.

As with all investments, historical data shouldn’t be taken as an indication of future performance. We can’t be held responsible for any financial decisions you make because of this information. Investing comes with risks, and there’s a chance you might not get back as much as you put in.

This document provides you with information about markets or economic events. We use publicly available information, which we believe is reliable but we haven’t verified the information so we can’t guarantee its accuracy.

This document belongs to HSBC. You shouldn’t copy, store or share any information in it unless you have written permission from us.

We’ll never share this document in a country where it’s illegal.

This document is prepared by, or on behalf of, HSBC UK Bank Plc, which is owned by HSBC Holdings plc. HSBC’s corporate address is 1 Centenary Square, Birmingham BI IHQ United Kingdom. HSBC UK is governed by the laws of England and Wales. We’re authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the PRA. Our firm reference number is 765112 and our company registration number is 9928412.